Yamana Gold (TSX: YRI, NYSE: AUY, LSE: AUY) is a sustainable gold and silver mining company based in Canada with five ongoing mining operations in Canada and South America. Yamana has seen a few volatile months. Since the beginning of the year, it has seen its price start at $5.19, drop to $4.90 and then make a steady climb up to a high of $7.88 on April 19th. It has since fallen to $6.34 and finally climbed back to its current $6.84.

Many investors may be wary of the company and have mistakenly chosen to hold off. Since the start of the year, these same investors who hesitated are likely down overall (the S&P500 dropping 15.7% and the TSX is down just over 3% YTD), but they would have seen a positive return on an investment in YRI of nearly 32%.

Yamana’s fundamentals are still strong, its long-term financials are aligned with ongoing market price movements, and the numbers for the first quarter were impressive. If more economic instability comes toward us, then gold will be an excellent investment, and Yamana may perform even better.

The Company

Yamana has investments in several ore-producing mines.

Canada Malartic

Yamana’s most significant asset is its 50% stake in the Canada Malartic mine. Malartic is Canada’s largest gold mine, and it’s a low-cost producer for Yamana, delivering 350K ounces of gold in 2021, and it’s expected to produce 320K ounces in 2022. The advancing large underground project has the potential to extend the mine’s life for decades.

Cerro Moro

This high-grade Argentinian underground and open-pit mine with exploration upside produced nearly 80K ounces of gold and 5.6 million ounces of silver in 2021 and expects to produce 95K ounces of gold and 5.3 million ounces of silver in 2022, with sustainable products that drive future growth.

El Peñón

The Chilian cornerstone underground mine has strong cash flow generation and a consistent track record of replacing mineral reserves for over 20 years. This mine produced 176K ounces of gold and nearly 3.6 million ounces of silver in 2021, expecting 170K ounces of gold and 4.2 million ounces of silver in 2022.

Jacobina

This top-tier Brazilian long-life underground mine has more than doubled production since 2014. In 2021 Jacobina produced 186K ounces of gold and expects to produce 195K ounces in 2022, with opportunities for further significant growth.

Minera Florida

The Chilian-established underground mine is transitioning to newer high-grade zones that will provide the foundation for future production increases and extend the mine’s life. In 2021 Florida produced 84K ounces of gold and is expected to produce 90K ounces in 2022.

These five projects make up Yamana’s base, and it plans to build on this strong portfolio with sustainable expansion at these properties as well as developing new mines at its current exploration and strategic asset properties.

Yamana has two properties that are currently being explored. Its Copper, Gold, Molybdenum, and Silver project called Mara in Argentina and its Wasamac gold project in Ontario, Canada; combined, these two exploration projects are estimated to produce 9.3 million ounces of gold and 11.7 billion pounds of copper.

Finally, Yamana has two strategic assets in Argentina and Chile that are at the near development stage, which will provide Yamana with years of new production potential.

Strategy

Yamana has a focus on sustainable mining that is often ignored in the industry. By thinking long term, they are giving themselves an advantage over other players in the space. The mining industry has a reputation for just taking from the earth and not caring who or what it hurts in the process, but Yamana has developed its program of Environmental Social and Governance (ESG) policies that it will continue to follow into the future.

At the core of Yamana’s ESG initiatives is ZERO. ZERO means zero health and safety incidents, zero community incidents, and zero environmental incidents across all of Yamana’s sites. ESG items that are related to health and safety, environment and community (HSEC) are managed at all levels, and employee compensation is tied to defined HSEC metrics.

Yamana’s Performance

When evaluating the gold and silver mining industry, it is of particular importance to pay attention to an established company’s Return on Equity (ROE). ROE is a useful tool that can be utilized to assess how effectively the company can generate returns on the investment received from the shareholders. Quite simply, ROE is a snapshot of the operating performance and the profit (Yamana has been profitable for 3 years) that the company is generating with respect to its shareholders’ investments.

Currently, Yamana’s ROE is sitting at 3.4%, double where it was eight months ago (1.7% in October 2021), and it has an earnings per share (EPS) of $0.15. However, this EPS is expected to grow. Seven analysts see Yamana’s EPS rising to an average of $0.30 in 2023.

While neither the current ROE nor EPS are outstanding for the industry, which has an ROE of around 15%, where Yamana shines is in its net income growth. In the past 5 years, Yamana has seen its net income grow a whopping 66%, while the industry has seen less than half of that (28.9%). The reasons for this increase are that Yamana is reinvesting a lot in itself with a high earnings retention and efficient management in place, evidenced by its ESG strategy. A growing net income means that Yamana is producing efficiently with its properties.

Yamana paid a dividend in 2021 and has also announced that it will be paying a 3-cent dividend at the end of June 2022, it has been paying a dividend for over 10 years.

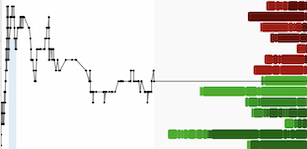

All told, the indicators for Yamana are positive for long-term success. Analysts collectively still have a target price of CA$9.17, which would be a 25.3% increase above its current $6.85 price.

Raymond James – Market Perform - C$8 Target

National Bank – Outperform - C$9.25

Berenberg Capital Markets – Buy - C$9.50 Target

Eight Capital – Buy - C$10.75 Target

When we look at the Gold price and the graph for Yamana side by side, we see a similar pattern with a bit less volatility.

With the ongoing war in Ukraine and supply chain issues that have continued since the fight against Covid began, combined with 40-year high inflation, gold is an asset that is turned to for its anti-inflation and stability properties. Having already gotten past its speculative phase and producing consistent profits, Yamana is a perfect hedge against these turbulent times and exactly why it has outperformed the broader markets and will likely continue to do so.

Recent News

In April, Yamana announced its first-quarter results with its low-cost performance seen across all properties with Jacobina and Cerro Moro standing out. This resulted in their operations driving a cash flow of $151.7 million. With the announced results, Yamana stated that it expects free cash flow to increase through the rest of the year, with the most robust free cash flow generation anticipated in its fourth quarter. This increase in cash will allow Yamana to continue its exploration activities without having to raise more cash to do so. This also is a good indicator that the dividend that it has paid will continue for the time being.

Summary

Yamana Gold is in an excellent position. It is an established gold producing firm that is producing its precious metals efficiently, and from this, seeing net profit and cash flow increases that are outpacing the rest of the industry. The five established and producing mines that Yamana is already running and the new projects, all with significant ore producing potential on the horizon, are expected to carry Yamana into the future. With the turbulent times at hand and the expectation that gold will remain an asset to hedge against inflation, Yamana is an intelligent play for long-term investment. The analyst consensus that the stock price is undervalued provides more incentive to buy in sooner rather than later.

#CEOStockResearchComp